A $50-million penthouse might be L.A.’s most expensive condo

[ad_1]

To unveil one of the grandest penthouses ever to be built in Los Angeles, its developers threw a little dinner party.

Two dozen of L.A.’s top real estate agents — the sunglasses-indoors kind who regularly appear on reality television — were tended to by a cadre of young women in identical cream outfits, hired for the evening to serve as “personal concierges.” Eight hundred gardenias were flown in from a San Francisco Bay Area flower farm, separated into individual vases and spaced exactly four inches apart on a long tablecloth-draped table. There was welcome Champagne and caviar blinis; a live singer in a glittery siren-red gown; and filet mignon with “caramelized heirloom truffle.”

Up for grabs: the city’s latest showstopping eight-figure penthouse, a decade in the making and finally for sale for $50 million off-market at a time when luxury condos in L.A. are more coveted than ever. If it sells at that price, it’ll break the county’s all-time condo sales record of $35 million, for a Century City penthouse that Candy Spelling bought in 2010 when she was looking to downsize. (Although, with another, even more expensive condo set to be listed this week, any new record might not stand for long.)

Across the hall, taking up the other half of the top floor of the new 8899 Beverly building in West Hollywood, is a second penthouse that will be available in the fall — or immediately, for a buyer willing to part with around $100 million for the pair. East and West were designed to be combinable into one uber-unit, which the developers say would make it the largest single-story penthouse in the world at nearly 20,000 square feet, including a wraparound terrace.

Guests at a dinner to reveal the East penthouse at 8899 Beverly included two dozen of L.A.’s top real estate agents.

(Brian van der Brug / Los Angeles Times)

A sizable marketing machine is now spinning up to get a blockbuster deal done soon, before looming economic concerns threaten to damp rich-buyer behavior. Developer Townscape Partners has been stoking anticipation for the penthouse for years and is looking to capitalize on L.A.’s scorching luxury condo market, which continues to rack up enormous sales even as real estate overall has started to cool.

The East penthouse is a steel-and-glass enclosure on the 10th floor with spectacular in-your-face views, nearly 14-foot-high ceilings, a private elevator, and massive sliding-glass windows and doors. A New York staging company was hired to outfit the space with luxe furnishings and artwork totaling “in the six figures,” one of the firm’s partners said, so a buyer could move right in if decorative tastes align.

If you’re talking about the ultra-luxury market — like over $5 million, $10 million — what you’re seeing is a buyer that collects residences almost like art.

— Fredrik Eklund, one of the listing agents for the East penthouse at 8899 Beverly

Historically, sprawling Los Angeles lagged behind other international cities when it came to expensive vertical living. If you were rich and looking to put down roots in the L.A. area, you wanted a mega-mansion in Malibu, Beverly Hills, Bel-Air or a similarly ritzy ZIP Code; paying many millions of dollars for shared walls and communal spaces was not the Southern California dream.

Buyers doubled down on stand-alone homes during the early stages of the pandemic, as airy indoor spaces, big backyards and ample distance from neighbors became even more important.

Months of restrictions and isolation led to a significant shift in mentality toward the end of 2020, real estate brokers said. Suddenly community, convenience and a carefree jet-setting lifestyle — aided by flexible remote-work policies and looser travel rules — were in high demand among the rich, and many gravitated toward the turnkey ease afforded by over-the-top condo buildings in desirable, centrally located neighborhoods.

“If you’re talking about the ultra-luxury market — like over $5 million, $10 million — what you’re seeing is a buyer that collects residences almost like art,” said Fredrik Eklund, one of the listing agents handling sales at 8899 Beverly. “They own maybe three or four of them in the best cities. They want to come and push a button and call the concierge and then they want to leave. And that’s a great life.”

“Personal concierges” await guests at a penthouse unveiling at 8899 Beverly in West Hollywood in June. Each pair of attendees was assigned one personal concierge for the evening.

(Brian van der Brug / Los Angeles Times)

In the first half of the year, 257 condos sold for $2 million or more in L.A. County, compared with 170 in the same time period last year and 75 in the first half of 2020, according to the Multiple Listing Service.

The number of condos in Greater Los Angeles that closed for more than $5 million in the second quarter rose 175% year over year, according to a report by Sotheby’s International Realty.

This month, a penthouse at the Pendry Residences West Hollywood closed for $21.5 million, making it the priciest condo sale this year and the fourth most expensive in the county’s history. A 2,681-square-foot two-bedroom unit in the same hotel-condo hybrid building sold for $13 million last summer, the highest price per square foot — $4,848 — in the history of L.A. condo sales.

A two-bedroom condo at Pendry Residences West Hollywood sold for $13 million last summer, a record $4,848 per square foot.

(Justin Coit)

As condos have grown in size and extravagance, their price tags have soared. There are currently 10 publicly listed condos for sale in Los Angeles for $10 million and up, and many more in development, ushering in a new trend in residential opulence in the city.

“We try to push the envelope and, God knows, try to push the pricing,” Eklund said.

8899 Beverly, like competing luxury buildings scattered around Los Angeles, comes fully loaded. Residents of the 40-unit main tower and eight adjacent townhouses have access to round-the-clock services, including valet, bellhop and doorman; a 12,000-square-foot outdoor area with a pool, hot tub, fireplaces, barbecue grill, covered dining area and dog park; a fitness center and yoga studio with an “a la carte personal trainer”; and a separate “auto stable” in the parking garage designed to showcase 16 exotic cars. An on-site restaurant with a private owner entrance is opening soon.

“A lot of it was trying to emulate as much as possible a single-family home while having all the benefits of high-rise living, which are views, security and amenities,” Townscape co-founder Tyler Siegel said.

8899 Beverly in West Hollywood is home to 40 luxury tower units, including a penthouse listed for $50 million, and eight stand-alone townhouses.

(Nils Timm)

Agents at the penthouse unveiling got one-on-one tours of the unit and property before dinner, a move designed to drum up interest among the industry’s most elite and well-connected.

“Who wants that $1.5-million commission?” Eklund said impishly at the start of the five-course meal, eliciting cheers at the prospect of such a substantial 3% cut.

The lavish and intimate June affair (“it was the cost of a small wedding,” one organizer said) was rare even in the flashy world of high-end real estate. One invitee said a gathering of that caliber of power brokers typically happens only at awards ceremonies or for reveals of $100-million-plus mansions — not condos.

Singer Natascha Bessez performs during a penthouse reveal dinner at 8899 Beverly in West Hollywood in June.

(Brian van der Brug / Los Angeles Times)

“Get the top agents to understand the building and to fall in love with the building because they’re the ones talking to the buyers,” said Jason Oppenheim, a real estate broker who also stars on the reality series “Selling Sunset.”

“A building like that, that is so luxurious, you really can specifically target the top agents, whereas maybe in a more generic building, you need to cast a wide net,” said Oppenheim, who was unable to attend because he was traveling. “Arguably, the agents at that dinner party are more than likely the agents that are going to bring in almost every buyer to that building.”

So who is the most likely buyer? Someone from out of town, agents speculated, maybe from the East Coast or abroad. Either way, a multi-home owner who will probably use the penthouse for only a few months of the year. It’s too expensive for a run-of-the-mill celebrity or professional athlete, one said, guessing it would go to a business tycoon.

This is someone who is going to walk in and is just going to want it and can afford it.

— Fredrik Eklund, one of the listing agents for the East penthouse at 8899 Beverly

What they agreed on is that buyers at this level are extremely sophisticated in their knowledge about real estate, the L.A. market and the latest economic trends and forecasts.

That could lead to tougher housing negotiations as consumers across all income levels contend with double-digit inflation, steep declines in the stock and crypto markets, and fears of an impending recession. On the morning of the penthouse reveal, the Federal Reserve raised interest rates by three-quarters of a percentage point, the largest increase since 1994; two days before, Wall Street fell into bear-market territory. On Wednesday, the Fed again raised interest rates by another three-quarters of a percentage point.

Asked if those factors were worrisome for luxury real estate agents, Cory Charlupski, one of three brokers tasked with selling the East penthouse, said: “Eff yeah.” Standing on the giant terrace after dinner, he said he expected clients to be more price-conscious and eager to drive a deal.

Townscape, however, said it intends to hold firm.

“Our buyers are relatively insulated from a lot of what you’re seeing out there,” Siegel said. “They may think they can negotiate better in a softer environment; I’m not sure we’re in that environment yet. We’ve got the staying power to make sure that we’re getting value for every one of our units. I think we’re in a position where we’re going to be patient if we need to be.”

Developers Tyler Siegel, left, and John Irwin on the terrace at 8899 Beverly.

(Brian van der Brug / Los Angeles Times)

Others said they believed a downturn would be mild, especially for the real estate industry, which is much more fundamentally sound than it was during the Great Recession. Wealthy clients, they predicted, would be largely unaffected.

“This is a cash buyer,” agent Tomer Fridman said at the event, adding that an uptick in interest rates “is not going to be an issue. There’s a lot of money in the world today.”

A lot of money — and not that many top-of-the-line penthouses available. That’s become a major selling point for developers: strategically marketing the units as one-of-a-kind masterpieces, created for a hyper-discerning buyer who wants something no one else has.

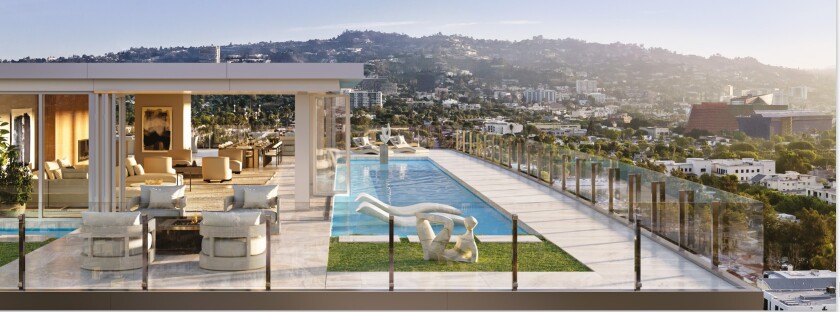

That’s evident at the Four Seasons Private Residences Los Angeles, which boasts a two-story, roughly 13,000-square-foot penthouse with its own rooftop pool named One L.A. that is available off-market for $75 million. It is believed to be the most expensive condo for sale in the county and will be publicly listed this week, real estate agent Billy Rose said.

“There’s only one city like Los Angeles — and there’s only one penthouse that reflects its distinct beauty and style,” reads the wording on the project’s website. “One L.A. Penthouse is destined to captivate the world. Reserved for only one.”

A rendering of the One L.A. penthouse at the Four Seasons Private Residences Los Angeles. At $75 million, it is believed to be the most expensive condo for sale in the county.

(Billy Rose / The Agency)

But that can also be a hindrance, said Lorenzo Esparza, founder of Manhattan West, a strategic investment firm in Century City. Super-expensive condos in Los Angeles are “uncharted territory,” he said, and he has been advising clients to exercise caution before buying them, especially as the economy shows signs of weakness.

“It’s very different than saying you’re buying on Billionaires’ Row in Manhattan where there’s a proven market for ultra-luxury condo buildings,” he said.

The eventual buyer of the East penthouse might not even care about comps or resale value or the economy, Eklund said.

“It’s an emotional buy, financial markets aside and calculations of capital and all those things,” he said. “This is someone who is going to walk in and is just going to want it and can afford it. This discussion with interest rates is a very important one and certainly relevant for maybe sub-$5 million, for normal people like myself, but this is a different kind of buyer.”

Times staff writer Jack Flemming contributed to this report.

[ad_2]

Source link